Basic Documents (For Everyone)

- Identity Proof: Aadhaar Card, PAN Card, Passport, Voter ID, Driving License (Any one)

- Address Proof: Electricity Bill, Water Bill, Telephone Bill, Ration Card, Bank Passbook, Passport (Any one)

- Age Proof: Birth Certificate, Aadhaar Card, PAN Card, Passport, Driving License, 10th Class Mark-sheet (Any one)

Property Documents

- Sale deed or allotment letter

- Approved building plan

- NOC (No Objection Certificate) from Society or Builder

- Detailed cost estimate for house construction

- Latest property tax paid receipt

- Ownership papers (title deed)

Income Documents

For Salaried People:

- Latest salary slips

- Form 16 or Income Tax Returns (ITR) for the last 3 years

- Bank statements for the last 6 months showing salary deposits

- Proof of any savings or investments (if any)

For Self-Employed People:

- Business address proof

- ITR for the last 3 years

- Balance sheet and Profit & Loss statement audited by a CA

- Business license or professional registration certificate

Additional Documents for NRIs (Non-Resident Indians)

Identity and Address Proof:

- Passport with visa stamps or PIO Card

- Proof of current overseas address (e.g., utility bill, government ID)

For Salaried NRIs:

- Recent salary slips or certificate

- Work permit/employment letter (translated if needed)

- Bank statements for the last 6 months showing salary deposits

- Form P60 or employment contract

For Self-Employed NRIs:

- Last ITR and financial statements

- Bank account statements for the last 6 months

- Business license or professional certificate

Property Documents for NRIs:

- Sale agreement or allotment letter

- Approved property plans

- Receipts for any payments made

- Clearance certificates (like an encumbrance certificate)

Other Important Documents

- Completed loan application form with 3 passport-size photos

- Loan account statement (if you have previous loans)

- Credit report (if available)

Note: Prepare these documents to ensure a smooth home loan application process.

The bank may also ask for more documents based on your situation.

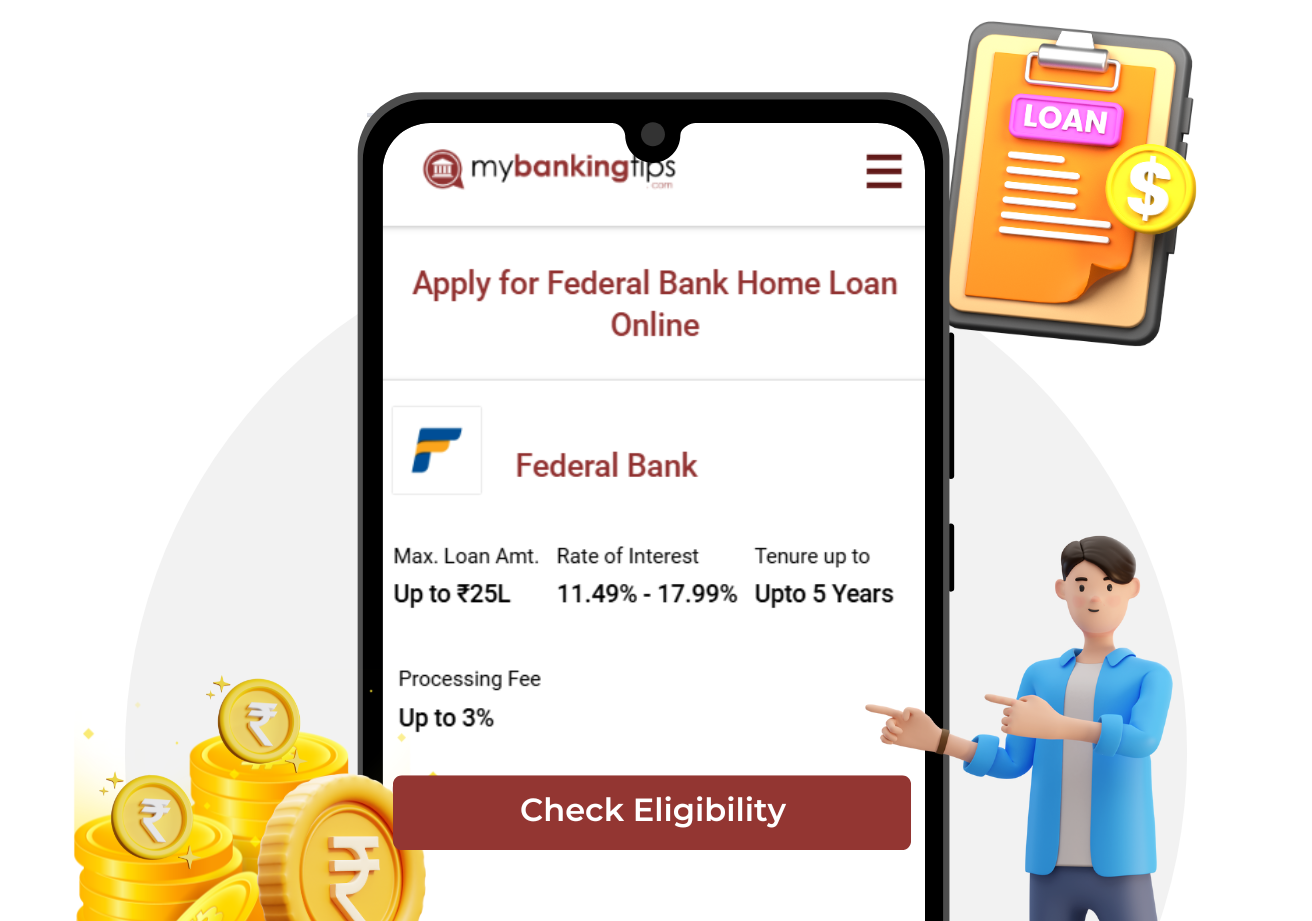

Interest Rate

Interest Rate

Loan Amount

Loan Amount

Tenure

Tenure

Processing Fees

Processing Fees